Did you start with a standard approach for investing?

Many investors start with “the usual”, maybe it’s a balanced mix of stocks and bonds from a popular index or target-date fund. It feels straightforward and low maintenance. Yet over time, clients often realize this cookie-cutter strategy falls short of meeting their specific needs. Life circumstances vary widely: one person might be saving aggressively for early retirement, another protecting wealth for heirs, and a third balancing growth with steady income. A one-size-fits-all portfolio rarely addresses these differences effectively, which is why customization has become a cornerstone of thoughtful investing.

Why do generic portfolios often miss the mark?

It all comes down to individual factors that drive long-term outcomes. Every investor brings a unique combination of goals, time horizon, risk tolerance, tax situation, and personal values. Ignoring these can lead to unnecessary volatility, missed opportunities, or suboptimal after-tax results. For example, two people of similar age might appear to need the same allocation, but one with a high tolerance for market swings and a long runway could benefit from greater equity exposure, while another nearing a major expense like college tuition might prioritize stability.

The core elements to consider when customizing include:

- Financial goals: Are you building wealth for retirement, funding education, buying a home, or preserving capital for legacy purposes? Clear objectives guide asset choices and allocation.

- Time horizon: How long until you need the money? Longer horizons generally allow more risk in pursuit of higher potential returns, while shorter ones favor preservation through bonds or cash equivalents.

- Risk tolerance: How comfortable are you with fluctuations? This includes both your emotional response to downturns and your financial capacity to absorb losses without derailing plans.

- Tax considerations: Where the money sits (taxable, IRA, Roth) and your current bracket influence decisions like municipal bonds for tax efficiency or Roth conversions.

- Personal preferences: Values-based exclusions (such as avoiding certain industries) or income needs can shape the mix.

How does customization work in practice?

Start by assessing these factors through a structured conversation with a financial advisor or a trusted questionnaire. From there, build an asset allocation that reflects them. A younger professional with decades ahead might lean 80-90 percent equities diversified across U.S., international, and emerging markets, plus some alternatives like crypto or alternative investments for resilience. Someone in their 60s focused on income could shift toward dividend-paying stocks, high-quality bonds, and fixed-income vehicles. Tools like direct indexing or separately managed accounts allow further tailoring, such as tax-loss harvesting or excluding specific holdings, while maintaining broad market exposure.

What are the benefits of a personalized approach to investing?

- Better alignment: The portfolio matches your life stage and priorities, increasing the likelihood you stick with it through market cycles.

- Improved risk management: Adjusting for tolerance and horizon reduces the chance of panic selling during volatility.

- Enhanced efficiency: Tax-aware strategies and goal-specific allocations can boost after-tax returns over time.

- Greater confidence: Knowing the strategy fits you personally makes it easier to stay disciplined.

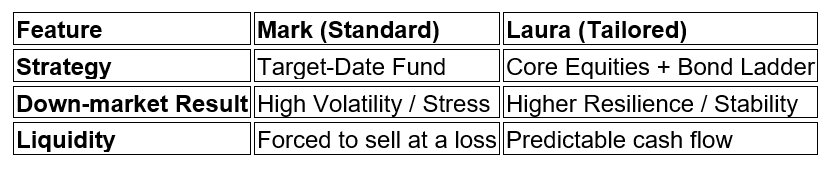

What would a standard approach to investing vs. a tailored approach look like in the real world?

Imagine two friends in their early 50s, both earning solid incomes and planning to retire in about 15 years. Mark chose a standard target-date fund that automatically adjusts over time. It provided simplicity and broad diversification, but when markets dipped sharply a few years ago, the heavy equity weighting caused more volatility than he was comfortable with. He also found himself short on reliable income as retirement drew closer, forcing him to sell assets at inopportune times to cover living expenses and help support his aging parents.

His friend Laura took a different path. She worked with an advisor to build a customized portfolio that reflected her specific situation. A core of diversified equities for long-term growth, a laddered bond strategy to generate steady income and reduce interest-rate risk, and a modest allocation to alternatives for added diversification beyond stocks and bonds. In her taxable accounts, she included municipal bonds to help minimize current taxes. When the same market downturn hit, her portfolio held up better due to the balanced structure. She had predictable cash flow to meet near-term needs without selling equities at a loss, and she felt more in control throughout the volatility. Over time, the tailored approach gave her greater peace of mind and flexibility to adjust as her circumstances evolved.

*TABLE TO BE INCLUDED FOR EASE OF COMPARISON

Does customizing mean constant tinkering or complexity?

The short answer is it doesn’t have to. It starts with understanding your situation and evolves as life changes. Periodic reviews, perhaps annually or after major events, ensure the portfolio remains relevant. In today’s environment, with access to sophisticated yet user-friendly tools and strategies, moving beyond generic models has never been more achievable.

Ultimately, a well-customized portfolio supports your unique path to financial security. It positions you to pursue goals with greater clarity and resilience. Working with an advisor to map out these elements can make the process straightforward and effective, helping every decision serve your bigger picture.

Disclosure: For illustrative purposes only. Asset allocation and diversification may not protect against market risk, loss of principal or volatility of returns.

Resources:

- https://www.finra.org/investors/insights/know-your-risk-tolerance

- https://www.fidelity.com/learning-center/personal-finance/risk-tolerance-time-horizon

- https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/ideas-and-insights/get-ready-for-2026-make-these-10-planning-moves-now

- https://www.blackrock.com/us/financial-professionals/insights/investing-in-2026