People are living longer than ever before. Advances in healthcare, better lifestyles, and medical breakthroughs mean many of us can expect to spend 20, 30, or even more years in retirement. While longer life is a blessing, it also changes the math of retirement planning. The same nest egg that might have lasted 20 years could fall short over 30 or 35. Adjusting your strategy now helps ensure your savings can support the life you want for decades to come.

Recent data highlights the urgency

Studies show that a significant portion of baby boomers face challenges with retirement readiness. For example, research from Vanguard indicates that only about 40 percent of younger baby boomers (ages 61 to 65) are on track to maintain their current lifestyle in retirement, with many facing an annual shortfall. Other reports point to even starker figures, with some estimates suggesting 20 to 30 percent of older Americans have little or no dedicated retirement savings, leaving heavy reliance on Social Security alone. These realities underscore longevity risk. One of the biggest challenges facing retirement planning today is the chance of outliving your money.

Traditional rules of thumb, like the 4 percent withdrawal rate, were designed around shorter retirement periods. With extended lifespans, those guidelines may need refinement to avoid depleting assets too quickly. The goal is to balance sustainable income with the flexibility to enjoy retirement while protecting against inflation, healthcare costs, and market swings over a longer horizon.

Key adjustments to consider include:

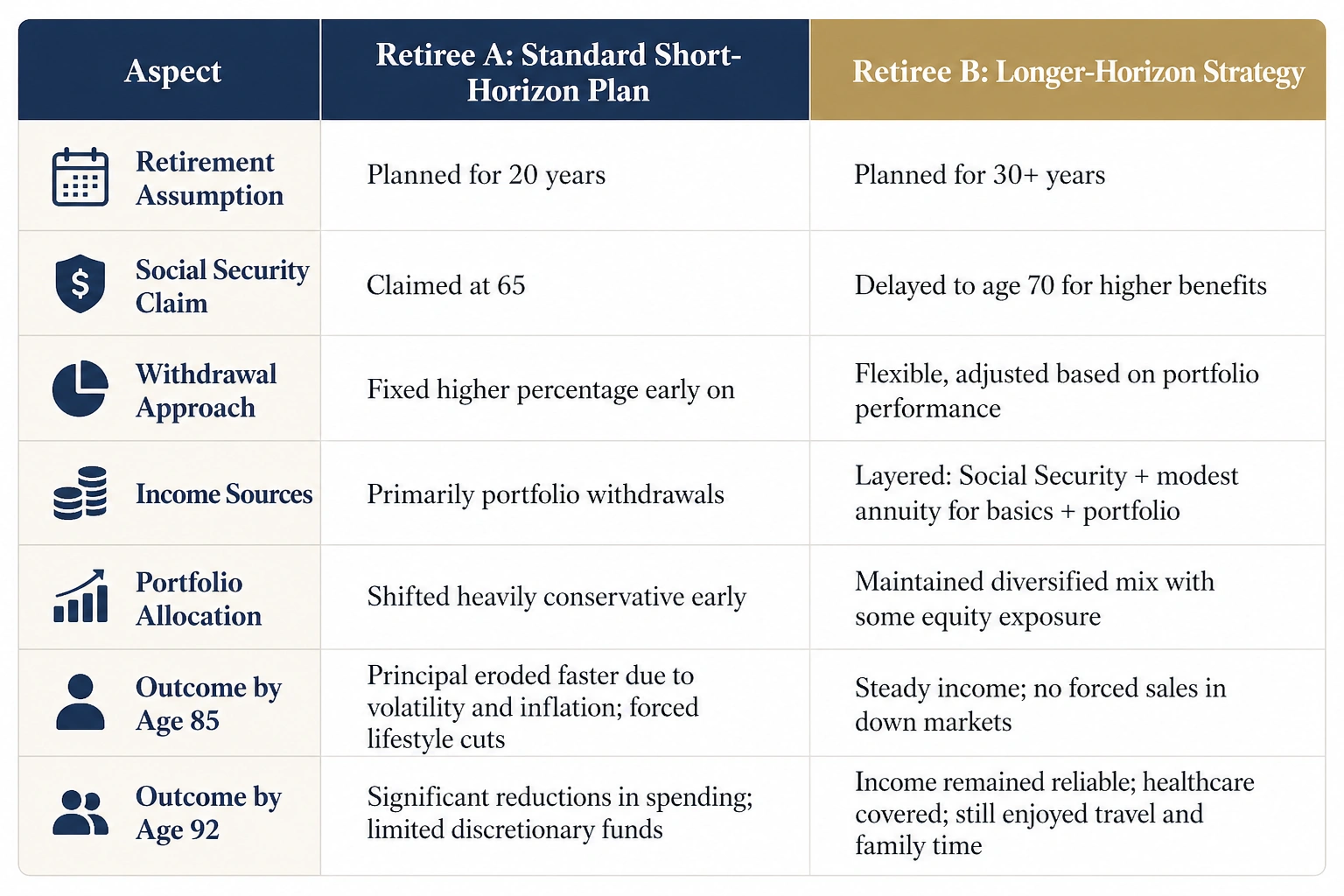

- Extend your planning horizon. Instead of planning for age 85 or 90, model scenarios out to age 95, 100, or beyond. This simple shift often reveals the need for greater conservatism in spending or a larger safety margin in savings.

- Reassess withdrawal strategies. A fixed percentage withdrawal can work early in retirement, but layering in more dynamic approaches helps later. For example, start with a moderate withdrawal rate and reduce it in down markets, or use a floor-and-upside method that helps guarantee essential expenses while allowing discretionary spending when portfolios perform well.

- Build multiple income streams. Relying solely on portfolio withdrawals increases risk. Incorporate additional sources like Social Security (delayed to maximize benefits), pensions if available, annuities for essential expenses, or part-time work in early retirement. These provide stability that equities and bonds alone cannot always deliver over decades.

- Prioritize healthcare and long-term care planning. Costs rise with age, and extended lifespans increase exposure to medical emergencies. Medicare covers quite a bit but not all, so consider supplemental coverage. A Health Savings Account (HSA) provides a vehicle for tax-advantaged medical savings. Additionally, long-term care insurance or hybrid policies can be considered to protect assets from extended care needs.

- Maintain growth potential. While preserving capital matters more as you age, staying too conservative can erode purchasing power against inflation over 30-plus years. A thoughtful allocation that includes equities, even in smaller proportions later in retirement, helps portfolios keep pace.

- Review and adapt regularly. Life expectancy estimates change with health, family history, and new data. Annual check-ins with a financial advisor allow adjustments as circumstances evolve, ensuring the plan remains realistic.

This example is for illustrative purposes only and does not represent the experience of any specific client or guarantee future results. Outcomes will vary based on individual circumstances, market conditions, and other factors.

Longer life offers more time for meaningful experiences, relationships, and pursuits. With thoughtful adjustments, your retirement strategy can match that extended timeline. It starts with realistic projections, diversified income sources, and ongoing reviews. Working with an advisor to tailor these elements to your health, goals, and resources helps create a plan that supports not just financial security, but a fulfilling life well into the future.

Resources:

- https://corporate.vanguard.com/content/corp/articles/us-retirement-outlook-our-2025-report-recap.html

- https://www.bankrate.com/retirement/retirement-savings-report

- https://www.ssa.gov/oact/population/longevity.html

- https://www.fidelity.com/viewpoints/retirement/planning-for-longer-life

- https://www.morningstar.com/retirement/how-plan-longer-retirement

- https://www.jpmorgan.com/insights/retirement/retirement-planning/living-longer-in-retirement